News Today(11/6): Eurozone Services PMI at 4:00 AM, Eurozone PPI at 5:00 AM. US Presidential Election results

Highlights:

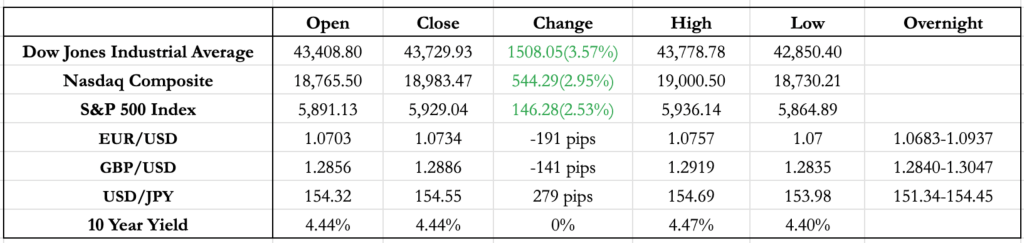

- By 7 pm ET, markets began to suggest that Trump was likely to win, and the dollar strengthened. EUR/USD fell 100 pips at first, then slipped another 100 pips by 10 pm as the outcome looked more likely. GBP/USD and USD/JPY followed similar moves, though GBP/USD showed slightly more resilience.

- Amid all the U.S. election noise, the Euro reported better-than-expected PMI Services and PPI numbers before Open, providing some positive support for EUR.

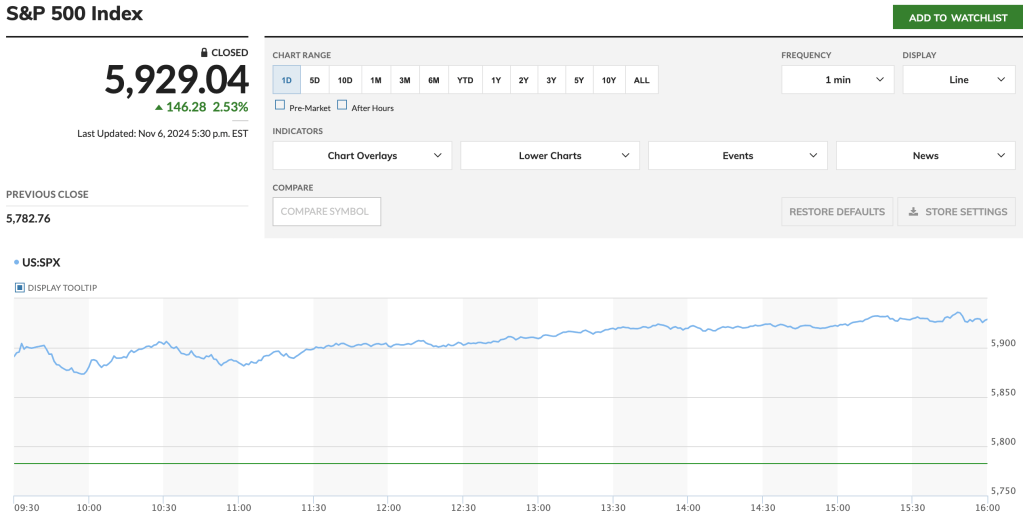

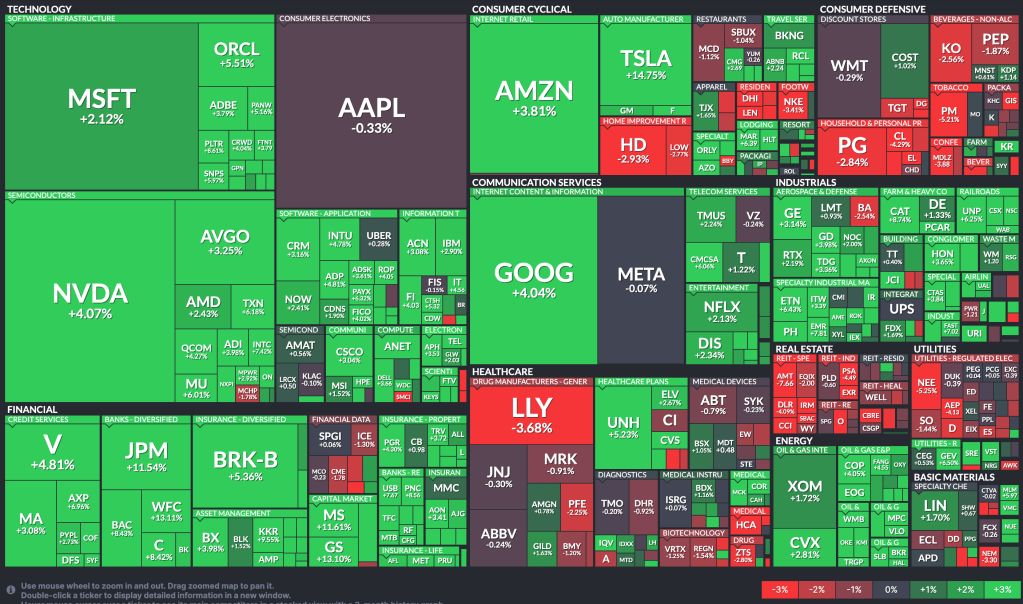

- U.S. markets opened with Trump’s win already confirmed, fueling a rally in stocks. Financials and Industrials surged the most, driven by expectations of corporate tax cuts and reduced regulation for banks. Meanwhile, Consumer Defensive, Utilities, and Real Estate sectors fell—Consumer Defensive and Utilities stocks likely because markets expect more money in circulation, and Real Estate due to limited room for rate cuts.

- Tesla (TSLA) gained 16%, while on the other end of the spectrum, renewable energy stocks struggled. The Renewable Energy ETF dropped 10%, while the Oil and Gas ETF surged 5%, reflecting expectations that Trump’s policies will favor the oil and gas sector more than renewables.

- Bond yields spiked, crossing their pre-NFP level after the Trump win confirmed, with yields rising from 4.28% to 4.4%. Markets are now anticipating that Trump’s inflationary policies could make it harder for the Fed to cut rates in the future.

FX Markets:

- EUR/USD saw its biggest one day drop of 191 pips with it breaching 1.07 just before the US open(7:22 AM). With Euro growth numbers coming in better now and with US rate cut tomorrow, we might see some relief tomorrow but I expect some volatility primarily caused by Trump’s speech and his comments on Tariffs.

- GBP/USD opened at 1.2856 and closed at 1.2886, down 141 pips from the previous day. Despite the overall market volatility surrounding the election, GBP/USD showed the most resilience of the major pairs. We might get more color on the UK budget as well the UK economy after Bailey’s speech tomorrow which is after the BOE rate cut decision where the expectation is of a 25bp rate cut.

- USD/JPY similar to EUR/USD also saw one of its biggest move of 279 pips, second only to the sharp decline during the Yen Carry debacle. Trump’s tariff policies are likely to affect China the most, but there could be spillover effects that impact Japan which could put further pressure on JPY. However, we will have to wait for the comments from new government to see if that would be the case.

- Based on past election patterns, the current trend tends to continue throughout the week. However, this could be interrupted by a likely 25bp rate cut tomorrow. While the rate cut itself most likely will be a dud, Powell’s comments could provide valuable insights into the Fed’s sentiment, which flipped to optimism after the last rate cut in September.

US Equity Markets

- The rise in tech stocks was surprising because tech usually does better with a Democratic win. But this time, the lack of major support or controversy from social media platforms might have helped the tech sector.

- Trump’s policies may help some companies, but it will take time for this to show. For now, I expect the market to trade sideways for the rest of the year, with growth and job numbers coming in as expected. The next few weeks will be interesting to watch as the market adjusts.

News Tomorrow(11/7): BOE Interest Rate Decision at 7:00 AM, BOE Governor Bailey speech at 7:30 AM, US Jobless Claims at 8:30 AM, Fed Interest Rate decision at 2:00 PM, FOMC Conference at 2:30 PM.

Sources: Marketwatch(https://www.marketwatch.com/), Reuters(https://www.reuters.com/), finviz(https://finviz.com/), fedwatch-tool(https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html), Tradingview(https://www.tradingview.com/), Sectorspdrs(https://www.sectorspdrs.com/sectorheatmap).

Leave a comment