News Today(11/7): BOE Interest Rate Decision at 7:00 AM, BOE Governor Bailey speech at 7:30 AM, US Jobless Claims at 8:30 AM, Fed Interest Rate Decision at 2:00 PM, FOMC Conference at 2:30 PM.

Highlights:

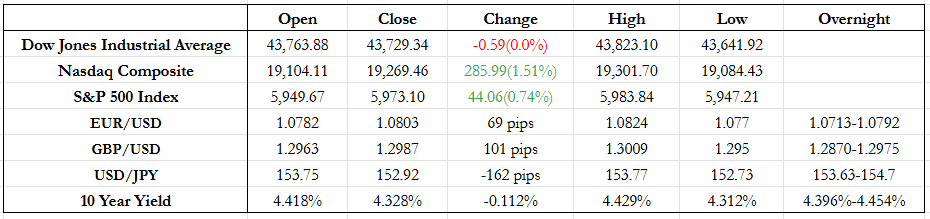

- The “Trump trade”-USD appreciation driven by expectations that his inflationary policies would push rates higher-is fading, suggesting it was flows driving the trend. All currencies recovered at least half of their post-election declines today, with GBP being the biggest gainer.

- US Initial Jobless Claims were in line with the expectation while continuing Jobless Claims slightly higher but no movement on that.

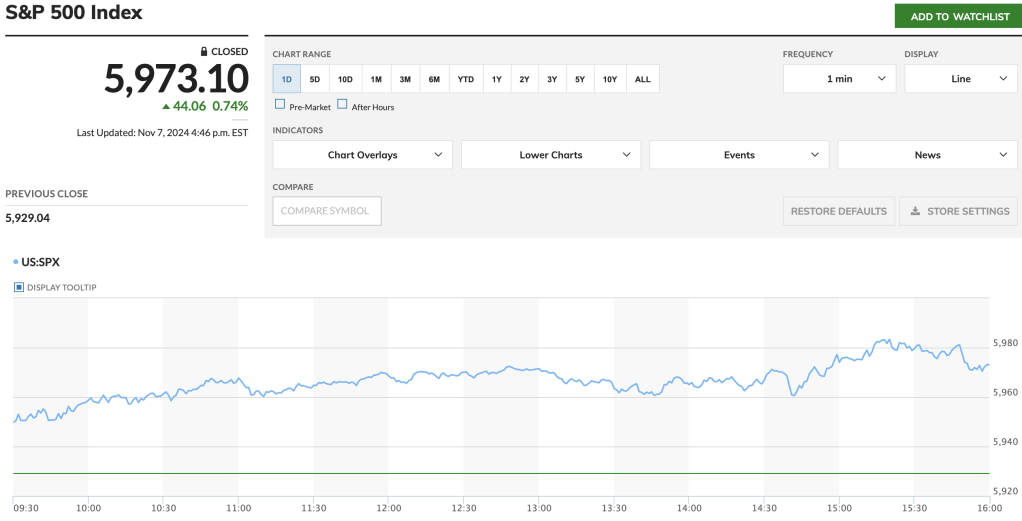

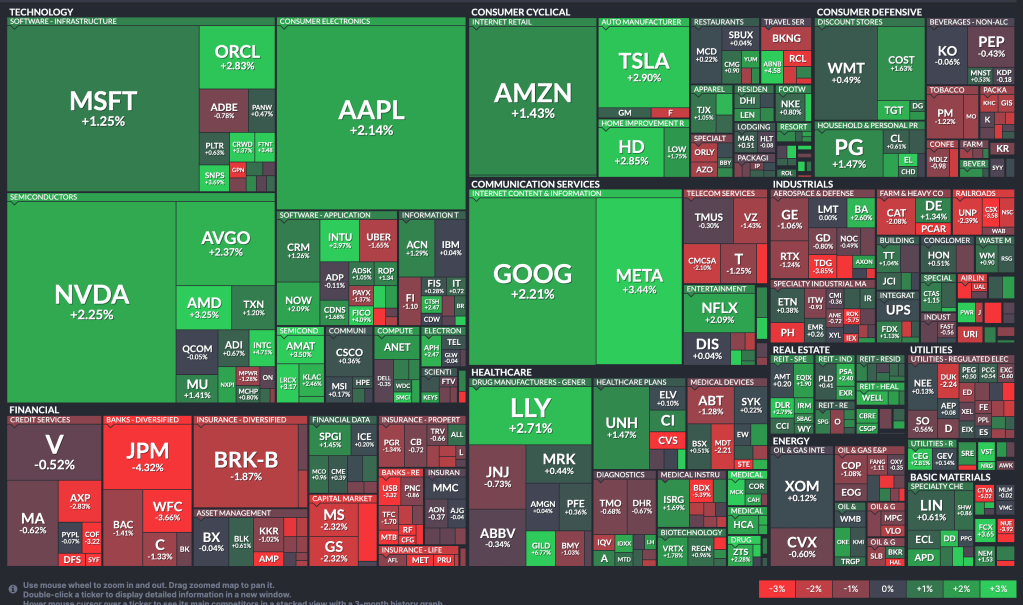

- Equities extended yesterday’s rally, with tech stocks leading the charge.

- GBP, notably the day’s biggest gainer, rose despite the BOE’s 25bp rate cut, as the bank hinted at caution over future cuts.

- The Fed also cut rates by 25bp, though this had minimal effect on markets. Powell’s comments remained optimistic about the U.S. economy, and he firmly expressed confidence in maintaining the Fed’s independence from government influence.

- Meanwhile, 10-year yields have nearly returned to pre-election levels, with no significant moves following the Fed’s rate decision and FOMC.

FX Markets:

- EUR/USD made a partial recovery from its US election-driven drop, gaining about 50 pips overnight and chipping away another 20 pips during the U.S. session. During the FOMC meeting, it had a 30-pip range, without a clear trend emerging from the announcement. With no major news expected tomorrow and no policy remarks from Trump, the unwinding of the Trump trade could continue. However, breaking above 1.09 might be challenging with the current momentum.

- GBP/USD continued to show strength which helped with a slightly hawkish stance from the BOE pushed it back to the pre-election levels. It briefly went above 1.30 during the U.S. session, but it didn’t have enough strength to stay there by the close. With lower trading activity expected on Friday and the unwinding of the “Trump trade” continuing, there’s a good chance it could close above 1.30 tomorrow.

- USD/JPY was the currency most impacted by the “Trump trade” flow, but it now seems to have returned to its pre-election trend of JPY weakening. This trend may get further support from market sentiment around potential tariffs on Japan that the Trump administration might implement again, similar to last time. Breaching 155 seems very likely, especially with CPI and PPI data next week.

US Equity Markets

- Tech stocks extended their rally from yesterday, with NVIDIA making history as the first company to reach a $3.6 trillion market cap.

- Bank stocks gave back some of their recent gains from yesterday, while consumer defensive stocks saw a little rebound from yesterday’s losses.

- It’ll be interesting to see how Apple manages new potential tariffs on China and how these might impact their growth forecasts under the new administration’s tariffs on China.

News Tomorrow(11/8): Michigan Consumer Sentiment at 10:00 AM

Sources: Marketwatch(https://www.marketwatch.com/), Reuters(https://www.reuters.com/), finviz(https://finviz.com/), fedwatch-tool(https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html), Tradingview(https://www.tradingview.com/), Sectorspdrs(https://www.sectorspdrs.com/sectorheatmap).

Leave a comment