News Today(11/13): CSCO(Cisco Systems) – 0.46% of S&P after Market Close.

BoE Monetary Policy Report Hearings around 8:00 AM, US CPI at 8:30 AM, Fed Speakers at 9:30 AM and 9:45 AM.

Highlights:

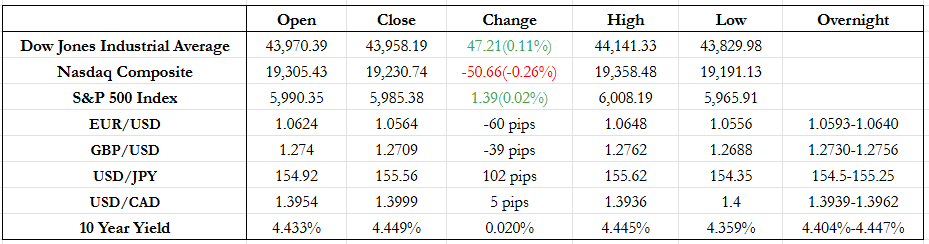

- U.S. CPI print matched expectations leading to smaller realized volatility at the number with most G10 currencies seeing 20-30 pips jump with USD depreciation briefly in the first five minutes after the release.

- But soon after, the trend of “Inflationary Pressure” continued, driving the USD higher with EUR/USD closed below 1.07 and USD/JPY climbed above 155.5.

- While expectations for a 25bp Fed rate cut jumped from 60% to 82%(Fed Watch tool which implies expectations from Bond Market) after the CPI data, the FX market told a different story, with the USD gaining strength after the print.

- Once again, all major currency pairs weakened further against the USD, with JPY closing 100 pips higher for a second consecutive day.

- Fed Presidents gave mixed messages: Kashkari said the neutral rate is higher now, hinting that the Fed might not need more rate cuts. But Logan and Musalem leaned toward more cuts, with Logan worried that inflation might take longer to drop back to 2%.

- Equities and Oil were unchanged primarily due to in line CPI print and inflationary pressure. Meanwhile, Bitcoin gains 1.25% closing shy above of $89000.

- I have similar expectations for PPI as I did for CPI yesterday. If inflation meets or beats expectations, it could further support the Trump Trade. However, to fully reverse the Trump Trade’s momentum, we’d need a significantly weaker-than-expected inflation print.

- Powell’s speech later in the afternoon tomorrow might also throw some more light on the current inflationary trend and how Fed plan to handle it.

FX Markets:

- EUR/USD continued to decline for the fourth day in a row. Although the CPI print provided some relief, briefly pushing EUR/USD to the day’s high, strong USD momentum returned after the market absorbed the data and Fed speakers’ comments, driving EUR/USD below 1.055. Last year’s low was 1.0460, and we might see that level tested if inflationary pressures stay high. The pair is also under pressure from weak growth (despite a recent pickup) and the ECB’s faster rate-cutting pace compared to the Fed, which widens the interest rate differential. Eurozone GDP could provide some relief, but a real trend reversal seems unlikely unless Eurozone GDP is strong and U.S. PPI and Jobless Claims data are unexpectedly weak.

- GBP/USD, like EUR, weakened for the fourth day in a row. Even though the BOE has been more cautious, USD inflation pressure is still strong. The UK budget has also added more volatility to the pair.

- USD/CAD closed at its highest level since COVID, at 1.4. It’s hard to see a reversal here, with Canada’s GDP still below 1% and the unemployment rate above 6%. USD/CAD has tried to break this level almost five times this year, and with this successful breakout, I expect the momentum to continue.

- USD/JPY has moved more than 300 pips since Friday’s close at 152.5. The momentum for JPY weakening can only be stopped if BOJ expresses concerns about the JPY or Trump comments about fewer tariffs for Japan. Although, the momentum for USD/JPY can only be stopped if the USD begins to depreciate sharply due to very weak inflation and jobs data in the future.

US Equity Markets

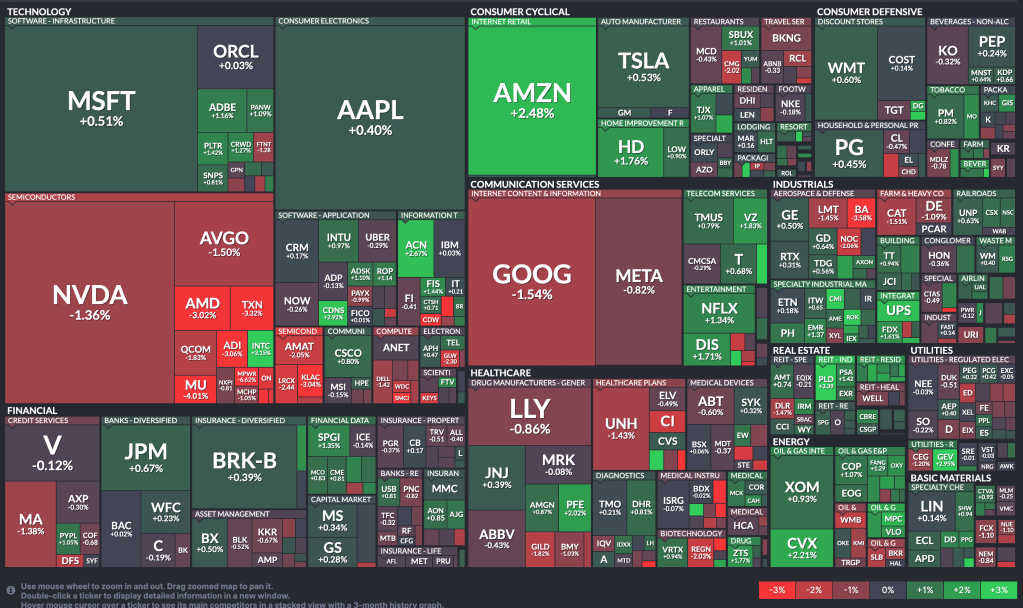

- Tesla saw some gains earlier in the day after Trump announced Musk as part of his cabinet, co-leading the DOGE (Department of Government Efficiency), but ended the day up just 0.5%.

- Dogecoin rallied 10% simply because the new department was named DOGE, and not for any other reason.

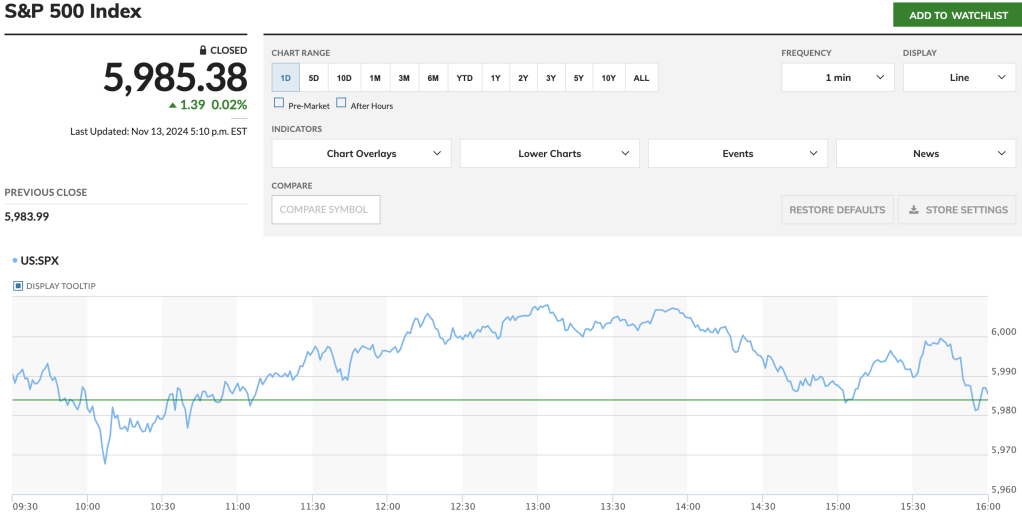

- A good CPI print allowed U.S. equities to open higher, but inflationary pressures pulled them back, causing them to close unchanged.

- The S&P 500 has gone above 6000 every day this week, but closing above 6000 has been tough. The index needs more momentum to keep going past 6000, which could come from Nvidia earnings on 11/20, followed by consumer retail stocks. However, retail stocks might struggle due to Home Depot’s comments on weak consumer spending and the CPI coming in line without signs of cooling.

News Tomorrow(11/14): DIS(Walt Disney) – 0.39% of S&P after Market Close

Eurozone GDP at 5:00 AM, US PPI + Jobless Claims at 8:30 AM, ECB President Lagarde’s Speech at 2:00 PM, Fed Chair Powell’s Speech at 3:00 PM and BOE Governor Pill’s Speech at 4:00 PM.

Sources: Marketwatch(https://www.marketwatch.com/), Reuters(https://www.reuters.com/), finviz(https://finviz.com/), fedwatch-tool(https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html), Tradingview(https://www.tradingview.com/), Federal Reserve Bank of St. Louis(https://fred.stlouisfed.org/series/CSCICP02CNM460S), scmp.com, econotimes.com.

Leave a comment