News Today(12/6): Germany Industrial Production at 2:00 AM, Eurozone Employment change and GBP at 5:00 AM, US NFP at 8:30 AM, US Michigan Consumer Sentiment at 10:00 AM and Fed Speakers at 10:30 AM, 12:00 PM and 1:00 PM

Highlights:

- BOE member Dhingra refrained from providing insights into further rate cuts, stating that “gradual policy changes are good on most occasions.”

- The Eurozone GDP print aligned with expectations, reinforcing positive growth prospects.

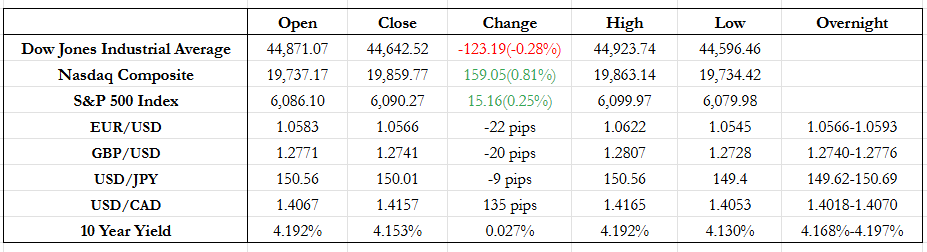

- The U.S. Jobs Report (NFP) came in line with forecasts (227K vs. 200K), with an upward revision to the abysmal previous month’s print (36K from 12K) due to storms and strikes. The unemployment rate was as expected (2.9%), though slightly higher than last month’s 2.8%.

- Market sentiment ahead of the NFP was divided, reflected in the wide range of estimates. This variance led to a ~30K (14%) higher reading being treated as in-line with expectations.

- The initial FX reaction was USD weakening, driven by a reduced interest rate differential due to the solidified expectations of a 25bp December rate cut. However, this faded within the first half-hour as USD’s growth differential regained dominance, supported by better U.S. consumer sentiment.

- Fed voting member Bowman provided mixed reactions to the NFP, stating that inflation remains too high, questioning the tightness of monetary policy, but also calling for cautious, gradual rate cuts. She also acknowledged the challenges in interpreting recent jobs data.

- Non-voting member Goolsbee expressed optimism about the economy and rate cuts, noting that rates remain “well above” the Fed’s dot plot. He reiterated expectations for inflation to hit the 2% target and highlighted the strength of the 227K NFP print.

- Conversely, voting member Hammack maintained a cautious tone, emphasizing the need for more evidence to confirm inflation’s decline toward 2%. He remarked that market expectations of a single rate cut by January (65% odds) align with his current outlook.

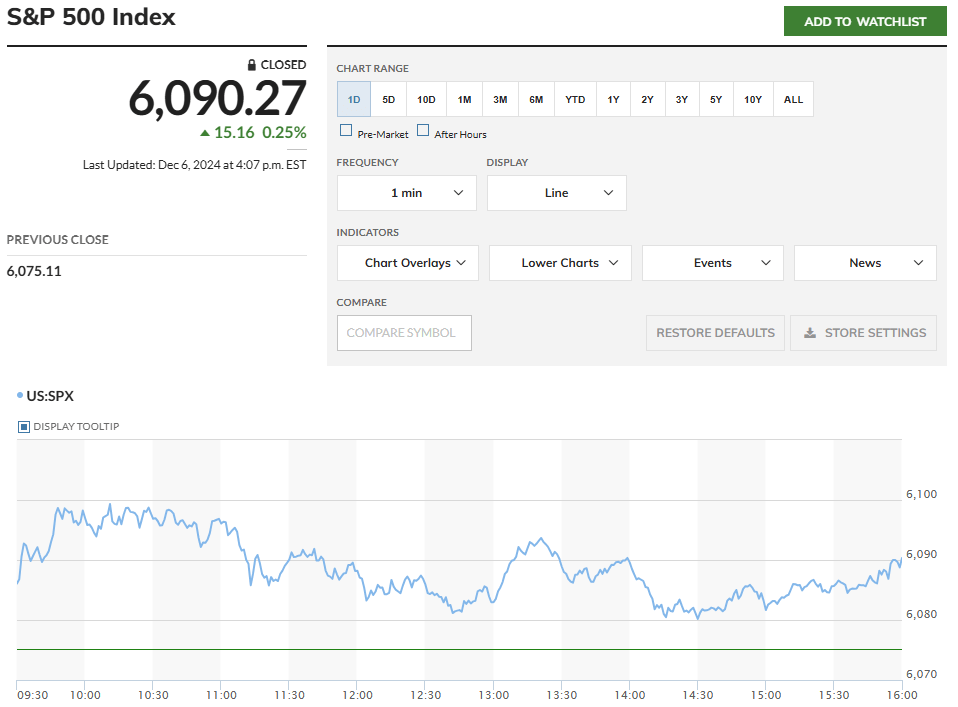

- The initial reaction in equities was highly positive, with indexes gaining approximately 0.25%–0.5% at the open. However, these gains were gradually eroded throughout the day. Nevertheless, the strong jobs report has reinforced the outlook for a continued rally compared to the previous session.

- Social media stocks, including Meta and Snapchat, surged after a federal appeals court upheld the ban on TikTok in the U.S. over national security concerns.

- Canada’s unemployment rate rose significantly above expectations (6.8% vs. 6.6%). Coupled with strong U.S. economic data, this drove USD/CAD to yearly highs and raised the odds of a 50bp rate cut to 80% from 55%.

Tomorrow Outlook:

- USD/JPY has been intriguing this week, trading within a range of 149 to 151 while repeatedly testing the 149 level. The pair has yet to fully price in the potential impact of future tariffs. While the BOJ’s interest rate hike and the Fed’s expected rate cut may temporarily support the yen, the growth differential is likely to outweigh the interest rate differential in the long term, potentially driving USD/JPY higher.

- Next week’s CPI and PPI reports (12/11 and 12/12) will be key economic events, determining whether equities can stage a final rally before year-end.

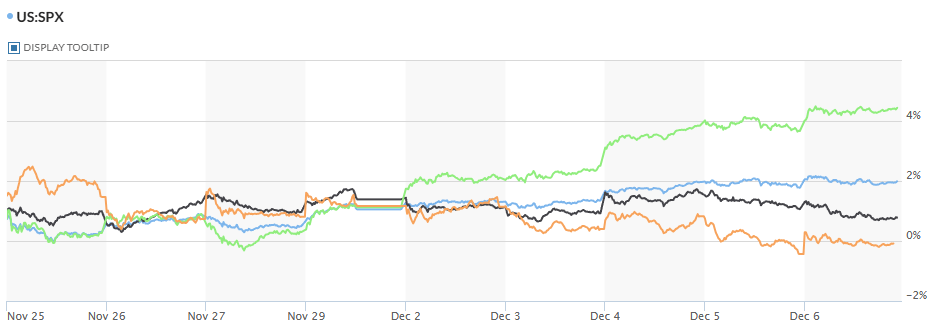

- Over the past two weeks, the Nasdaq has delivered significant outperformance compared to the S&P 500, Dow Jones, and Russell 2000. However, with the U.S. economy demonstrating resilience and a December rate cut nearly guaranteed, small-cap stocks are poised for potential outperformance in the near term.

News Tomorrow(12/9): Japan GDP at 6:50 PM(12/8), Oracle(ORCL) – 0.58% of S&P500 earnings after market close

Sources: Marketwatch(https://www.marketwatch.com/), , Reuters(https://www.reuters.com/), finviz(https://finviz.com/), fedwatch-tool(https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html), Tradingview(https://www.tradingview.com/), Sectorspdrs(https://www.sectorspdrs.com/sectorheatmap)

Leave a comment