News Today(12/18): UK CPI & PPI at 2:00 AM, Fed Interest rate decision at 2:00 PM, FOMC Conference at 2:30 PM and BOJ Interest rate decision at 10:00 PM

Highlights:

- Better-than-expected U.K. CPI data was released today, but it had no significant market reaction. Overall, currency pairs traded within tight ranges as markets awaited the Fed’s decision.

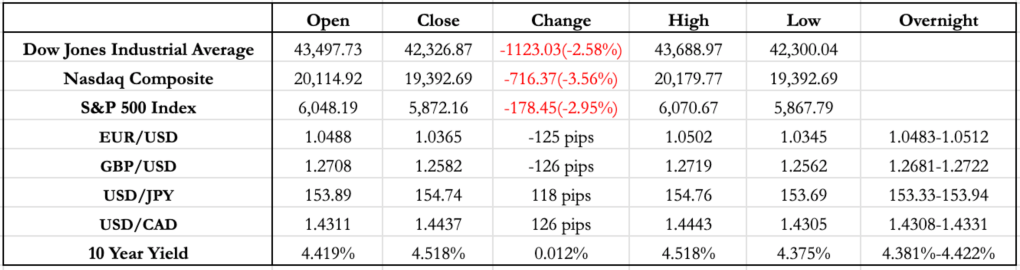

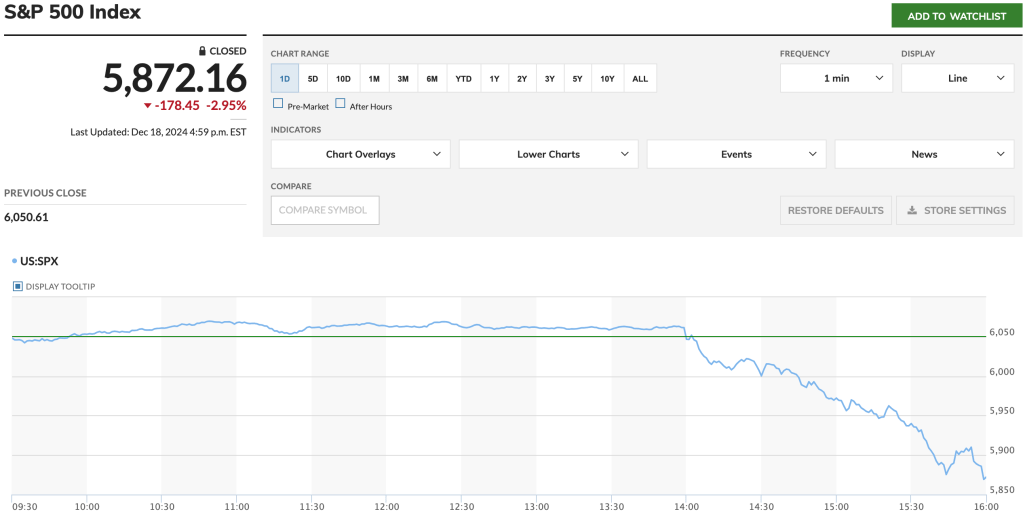

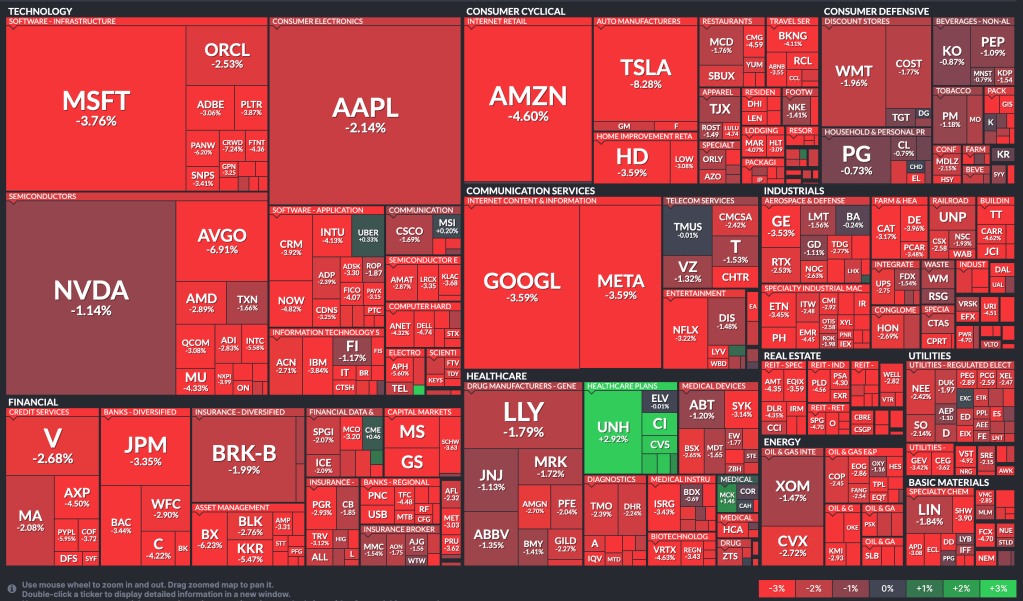

- The Fed announced a 25bp rate cut this month which was the market consensus but reduced its projection for next year’s rate cuts from four to two. This shift led to nearly a 1% drawdown in equities and a 20-30 pip appreciation in the USD.

- During the FOMC press conference, Fed Chair Powell made bearish remarks, emphasizing that inflation remains elevated with significant uncertainty surrounding its trajectory. He reiterated that future inflation data would play a crucial role in determining the Fed’s rate-cutting cycle. These comments added further pressure on equities, which closed the day down 3%, while the USD strengthened by more than 100 pips against all major pairs.

- Additionally, the 10-year yield surged, closing 12.5bp higher on the day, marking a 25bp increase since the start of the month.

- Some of the Powell comments during the FOMC conference were:

- Today was a closer call

- We know we are 100 basis points closer to neutral; no real certainty about long run neutral rate

- From this point forward, appropriate to move cautiously; risks balanced

- Repeats inflation has eased significantly but remains somewhat elevated relative to long-term goal

- Forecasts for inflation higher this year headed into end of year; could be single biggest factor affecting rate outlook

- Uncertainty about inflation higher; some FOMC members began trying to include different fiscal policy re inflation outlook

- To cut further after this point, will look for further progress on inflation

- Premature to assess impact of tariffs

- We are not allowed to own Bitcoin; not looking for a law change

- Although the Fed projects 2 rate cuts next year, bonds (as indicated by the FedWatch Tool) are pricing in only 1 for the entire year.

Tomorrow Outlook:

- Although Powell did not explicitly say that Trump’s policies will lead to inflationary pressure, he did mention that the current “scenario” runs the risk of higher inflationary pressure, which led to their stance of slow and gradual easing.

- There wasn’t a significant reaction immediately after the interest rate decision. However, during and after the FOMC conference, the market priced in significant interest rate differentials across all the G10 pairs, with EUR/USD bearing the most brunt.

- EUR/USD now faces clear downside pressure as both the interest rate and growth differentials tilt in favor of the USD. Only significantly weaker U.S. growth data or substantially stronger Eurozone growth data could shift the balance – and even then, it would likely only impact the growth rate differential. The ECB’s stance on further easing has been mixed but leans toward additional rate cuts, which already widens the USD interest rate differential. EUR/USD has touched 2-year lows today, which could provide additional momentum to push the pair further down.

- GBP/USD also weakened by more than 100 pips. But given the BOE’s conservative stance on rate easing and their better-than-expected to in-line recent growth and inflation data, we might see a strong reversion tomorrow. With the BOE rate decision tomorrow, if they continue with their conservative stance, we could see a bounce-back. However, anything other than that, and GBP/USD might test yearly lows of 1.2350.

- USD/JPY weakened by more than 100 pips but showed the most resilience compared to other pairs. With the BOJ interest rate decision later tonight, USD/JPY is primed to break 155 and potentially move further if there is no rate hike (10% odds of a hike). However, if the BOJ signals a willingness to hike in response to steep Yen depreciation, it could cap the USD/JPY movement. On the other hand, if there is no rate hike and no comments on Yen stabilization or any imminent rate hike, USD/JPY could target 157.5 before the year-end.

- Equities experienced a significant drawdown today, erasing half of the post-election gains. After the S&P 500 broke the 6000 level, it triggered some stop-losses, leading to further selling pressure, which may have caused an overreaction. I see a 1-1.5% chance of a bounce-back until the year-end.

News Tomorrow(12/19): BOJ Interest rate decision at 10:00 PM, BOE Interest rate decision at 7:00 AM, US GDP and Initial Jobless Claims at 8:30 AM, Existing Home Sales at 10:00 AM

Sources: Marketwatch(https://www.marketwatch.com/), , Reuters(https://www.reuters.com/), finviz(https://finviz.com/), fedwatch-tool(https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html), Tradingview(https://www.tradingview.com/)

Leave a comment