News Today(1/28): ECB President Lagarde Speech at 12:00 PM, BOJ Monetary Policy minutes at 18:50 PM

Highlights:

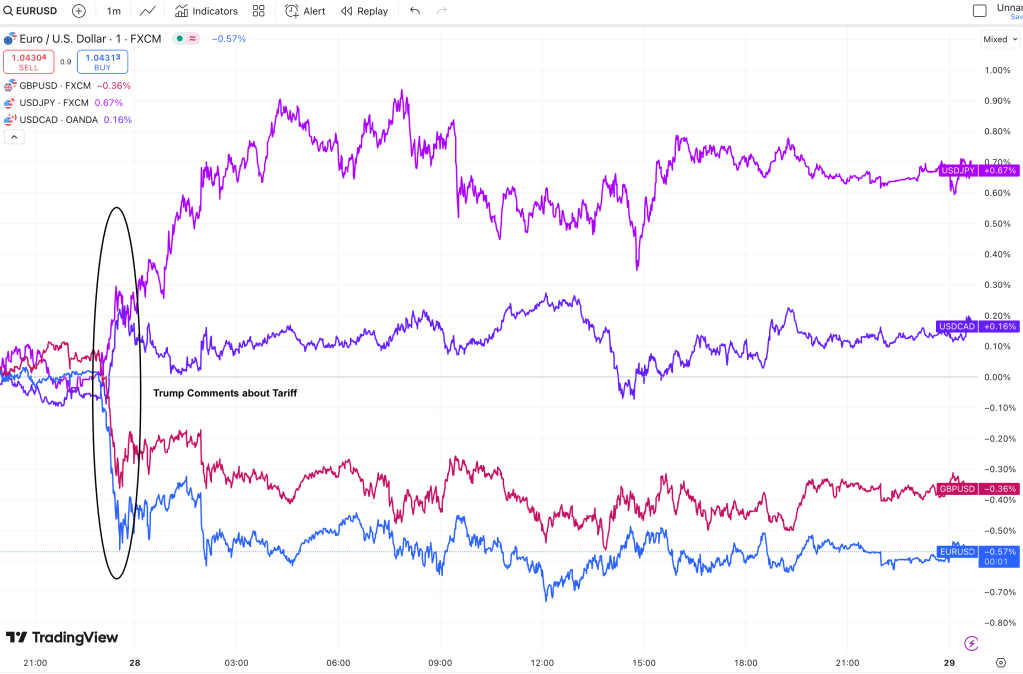

- Trump reiterated plans to impose tariffs specifically on computer chips, pharmaceuticals, and steel, which led to USD appreciation, as shown in the plot below.

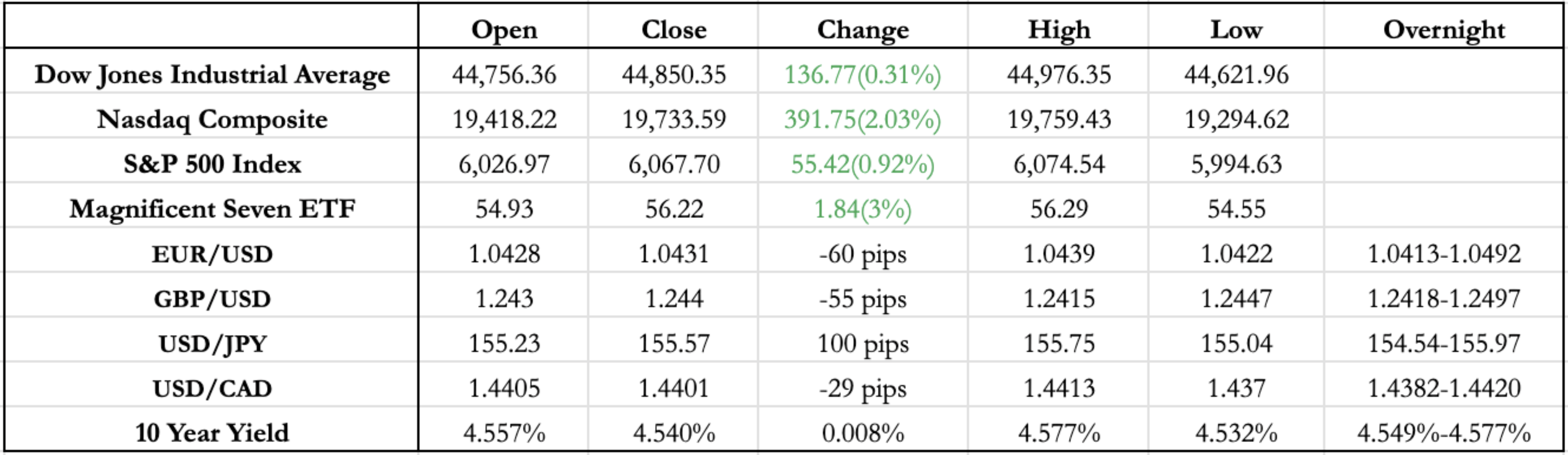

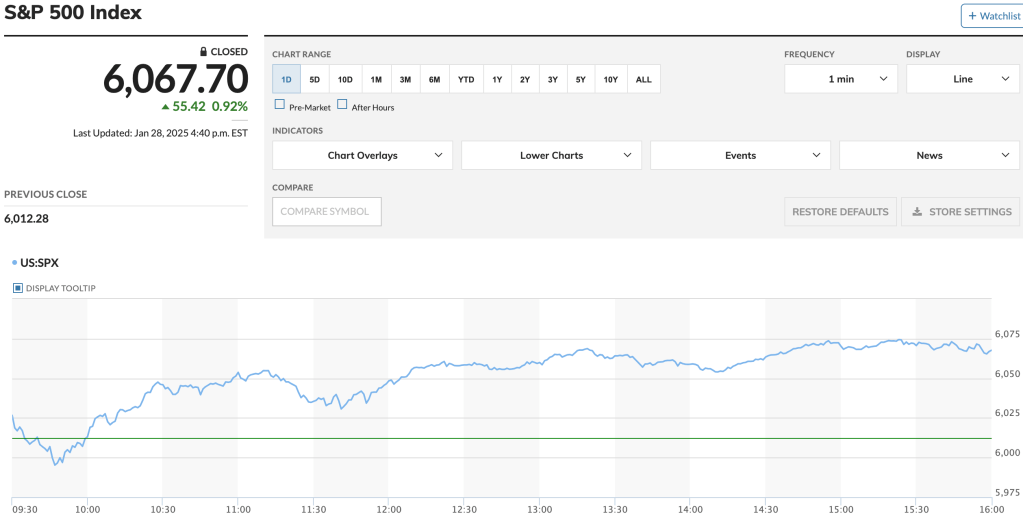

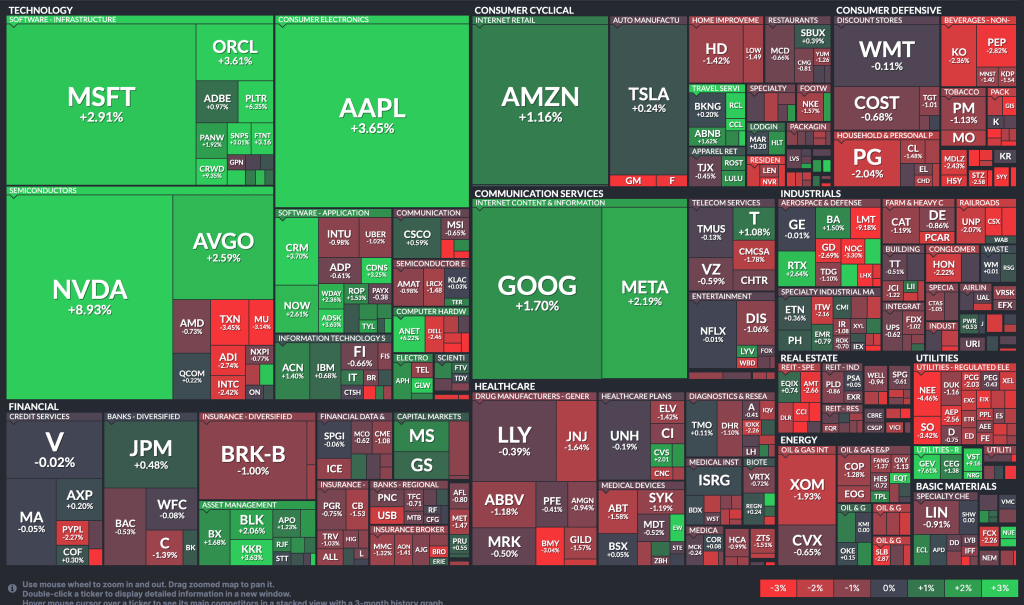

- After yesterday’s panic-driven tech selloff following DeepSeek’s reports, markets have bounced back, recovering more than half of the previous day’s losses, with Nvidia leading the charge, up 8%.

- OpenAI CEO Sam Altman weighed in on DeepSeek, expressing support for healthy competition in the industry – a sentiment Trump echoed after yesterday’s market close.

- The FX market traded in a tight range today, following the USD movement sparked by Trump’s tariff comments. So far this year, most market moves have been driven by tariff threats rather than the broader underlying macro environment.

Outlook:

- We have 10% of the S&P 500’s weighted earnings reporting after the close tomorrow, including Meta, Microsoft, and Tesla. Regardless of the actual earnings numbers, the forecasts and commentary for the next quarter will play a key role in shaping the broader market trend. Any revisions to prior guidance citing tariffs as a factor will also provide insight into Big Tech’s sentiment surrounding the proposed tariffs.

- The rate pause decision tomorrow is nearly certain (99.5%), but any indication of a shift toward a less hawkish stance could push yields lower. Over the past two months, major macroeconomic indicators (CPI, PPI, Core PCE, GDP, and NFP) have largely come in line with or better than expectations, strengthening the case for a rate pause given the resilience of the economy. However, the recent weakness in Retail Sales and ADP Employment (Non-Farm Private Employment) could be addressed during the FOMC conference, potentially reinforcing expectations of two rate cuts this year.

- Similarly, while Eurozone macroeconomic data has been consistent, it remains weaker relative to the U.S. economy. The ECB’s shift to a more dovish tone during its last meeting has done little to support EUR/USD. Although the pair is trading 300 pips above its yearly low of 1.0180, the risk of the Euro breaking parity (1.0) remains a possibility.

- USD/JPY, which had been relatively stable amid tariff-driven volatility and reached a yearly high of 153.8 yesterday following the BOJ’s 25bp rate hike on Friday, lost nearly 100 pips after Trump’s tariff comments. Given that the BOJ hike failed to significantly strengthen the yen, if the Fed maintains its hawkish tone in tomorrow’s FOMC commentary, USD/JPY could resume its upward drift toward 160.

News Tomorrow(1/29): BOE Governor Bailey Speech at 9:15 AM, BoC Interest rate decision at 9:45 AM, BoC Press Conference at 10:30 AM, Fed Interest rate decision at 2:00 PM, FOMC Press Conference at 2:30 PM, Meta(2.82% of S&P500), Tesla(2.18% of S&P500), Microsoft(6.34% of S&P500), and IBM(0.41% of S&P500) Earnings after market close

Sources: Marketwatch(https://www.marketwatch.com/), , Reuters(https://www.reuters.com/), finviz(https://finviz.com/), fedwatch-tool(https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html), Tradingview(https://www.tradingview.com/)

Leave a comment