News Today(11/11): Veterans Day: Bond Market Closed

Highlights:

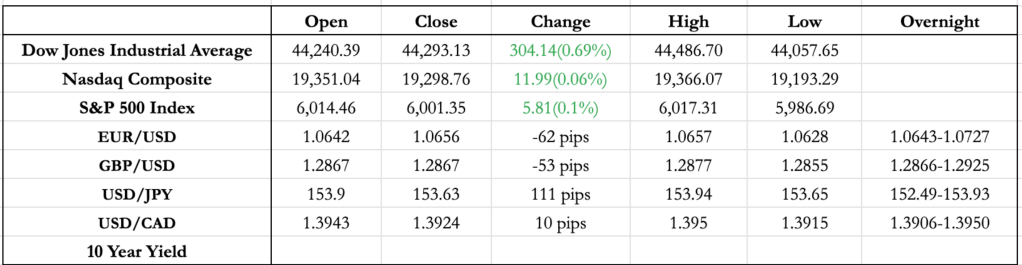

- USD Rally Continues: The dollar strengthens further, with the euro bearing the brunt, breaking below the U.S. election low and closing under the 1.07 level. Meanwhile, GBP is showing the most resilience among major currencies, holding its ground better than the euro.

- CAD at Two-Year Lows: The Canadian dollar is close to the two-year low, facing risks from potential Trump tariffs and lower oil prices, Canada’s largest export.

- Crude Oil Drops Further: Oil prices dropped another 2%, now at $68. This slide is driven by Trump’s backing for increased U.S. oil production, as well as China’s recent stimulus package, which fell short of expectations and could signal weaker oil demand from the world’s second-largest consumer.

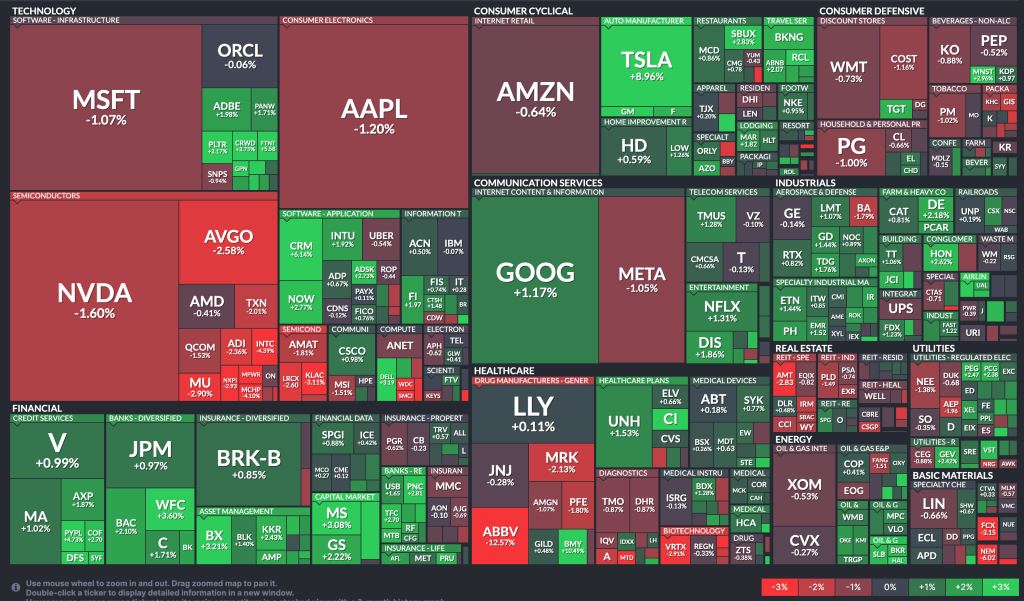

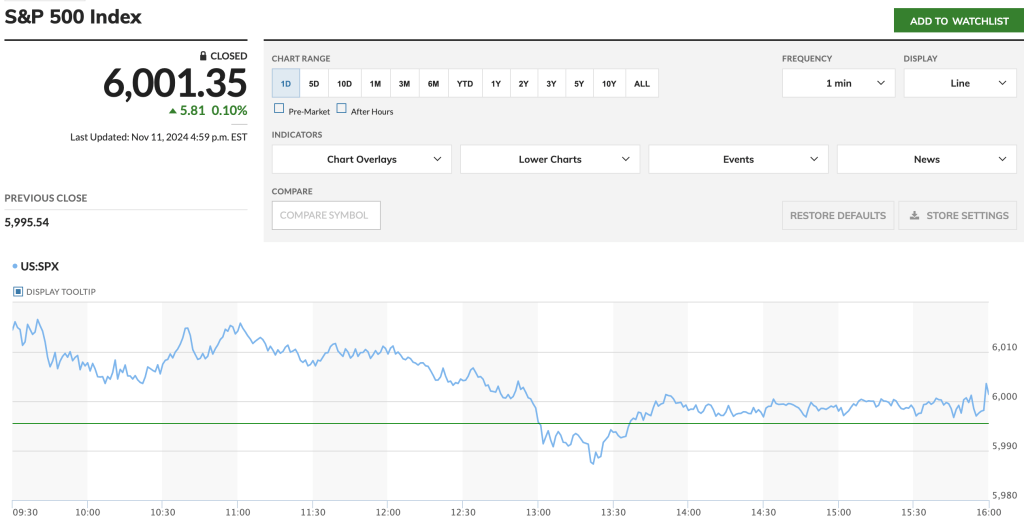

- S&P 500 Crosses 6,000: The S&P 500 closed above the 6,000 mark. Stocks tied to the “Trump Trade” theme—Tesla, banks, and industrials—continued to rally, with Tesla climbing another 9%.

- Bitcoin Surges: Bitcoin hit an all-time high, closing the U.S. session at $88,000, soaring as Trump’s support for cryptocurrency and potential crypto-friendly regulations boost market optimism.

- 68% chance of 25bp rate cut in December(12/18) by Fed according to the FedWatch tool.

Deep Dive: China Stimulus

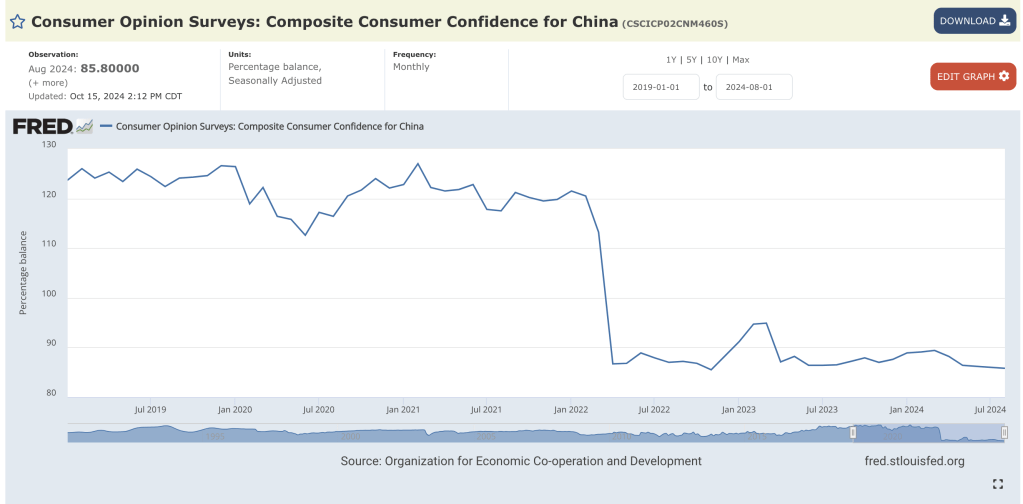

- China is currently facing deflation, meaning the prices of goods and services are decreasing. The primary reasons for this are weak consumer confidence, which remains far below pre-COVID levels, and the struggling real estate market. The real estate sector is suffering due to over-leveraging by developers, which has stalled many projects and negatively impacted related industries such as construction materials and household appliances.

- There was some temporary relief for the Chinese markets when the government announced a stimulus package. However, this relief was short-lived. The stimulus, which was released last week, totals $1.07 trillion (6% of China’s GDP). The main focus of the Chinese government’s stimulus was the real estate sector, for which they introduced measures like cutting mortgage debt servicing, issuing bonds for local government spending, and providing financial support to state-owned banks. Additionally, two major financing facilities worth $112 billion have been set up to stabilize the stock market. One of these is a swap scheme, which allows brokerages and fund managers to exchange stock holdings for liquidity, while the other allows financial institutions to borrow funds to support stock buybacks.

- This comprehensive stimulus was still considered conservative by investors and analysts, with the common sentiment being that it isn’t enough to revive growth. Additionally, the potential impact of Trump’s tariffs was not factored into the analysis, which could further weigh on China’s economic recovery

FX Markets:

- EUR/USD continued its decline, breaking below the US election low of 1.0685 and closing at 1.0656. Most of this drop happened during the overnight session, with it opening at 1.0642 and trading in a tight range during the US session. While Eurozone growth data has been improving recently, there are concerns that new U.S. tariffs, especially under a new government, could hurt the EU the most, as it is the largest exporter to the U.S. This could push the ECB to cut rates further.

- GBP/USD opened and closed at 1.2867, with a tight range of just 22 pips during the US session. Similar to EUR/USD, most of the movement happened in the overnight session. The British pound has shown notable resilience against the USD, largely due to inflationary concerns surrounding the new UK budget. These concerns have pushed Gilt yields higher, which implies it would be harder for the BOE to cut rates.

- USD/JPY has surprisingly shown some resistance to the dollar, likely due to bullish bets placed by speculators on the yen. The high during the US elections was 154.5, which remains a key resistance level. If it surpasses this level, we could see USD/JPY breaching 157.5 soon, unless the BOJ intervenes.

- We have a lot of inflation data coming this week, starting with the U.S. Consumer Price Index (CPI) on November 13, followed by the Producer Price Index (PPI) on November 14, and Retail Sales on November 15 along with Eurozone CPI and GDP, as well as the UK’s GDP. Although Trump policy rhetoric might overpower the USD prints but Euro and UK numbers might give some relief to EUR and GBP respectively if they come in better than expectation.

US Equity Markets

- Tesla gained 8% due to heavy near-term call option buying. As options sellers (market makers) hedge their delta risk, they buy the stock, which pushes the price up. This drives the stock higher.

- It’s clear that Trump’s policies will benefit many sectors and companies, but we’re entering a point where we may be overpricing those benefits. These policies also carry the risk of higher inflation, and if that cycle takes hold, it could lead to stagflation, which would be hard to avoid.

News Tomorrow(11/12): HD(Home Depot) – 0.79% of S&P before Market Open., SPOT(Spotify) after Market Close.

Germany CPI at 2:00 AM, UK Clairmont Change(~Jobless Claims) + UK Unemployment Rate at 2:00 AM. Fed Speakers at 10:00 AM, 10:15 AM and 2:00 PM.

Sources: Marketwatch(https://www.marketwatch.com/), Reuters(https://www.reuters.com/), finviz(https://finviz.com/), fedwatch-tool(https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html), Tradingview(https://www.tradingview.com/), Federal Reserve Bank of St. Louis(https://fred.stlouisfed.org/series/CSCICP02CNM460S), scmp.com, econotimes.com.

Leave a comment