News Today(12/12): European Central Bank(ECB) Interest rate decision at 8:15 AM, US PPI at 8:30 AM, ECB Press Conference at 8:45 AM, US Treasury 30-Year Note auction at 1:00 PM and Broadcom(AVGO) earnings – 1.56% of S&P500 and Costco(COST) earnings – 0.86% of S&P500 after market close

Highlights:

- The Swiss National Bank (SNB) unexpectedly cut rates by 50 basis points overnight, causing the Swiss franc (CHF) to weaken by 60 pips immediately after the announcement. This weakening trend continued well into the U.S. session.

- The European Central Bank (ECB) cut rates by 25 basis points, as expected, resulting in no significant market reaction. During the subsequent press conference, the ECB President made several insightful comments, including that growth is losing momentum, inflation risks are two-sided, and there had been discussions about a potential 50 basis point cut during this meeting.

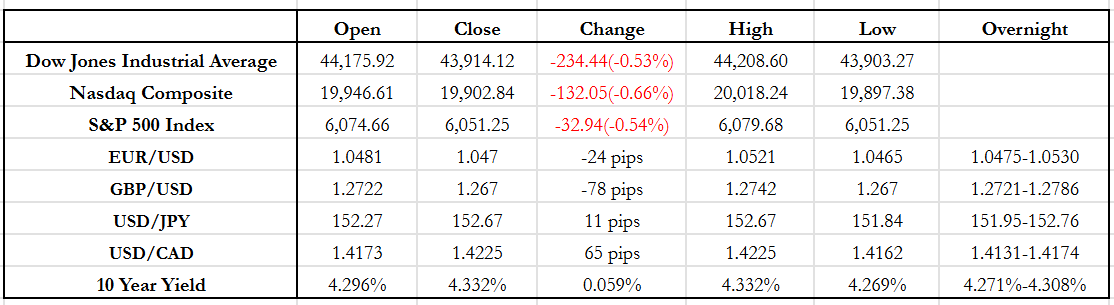

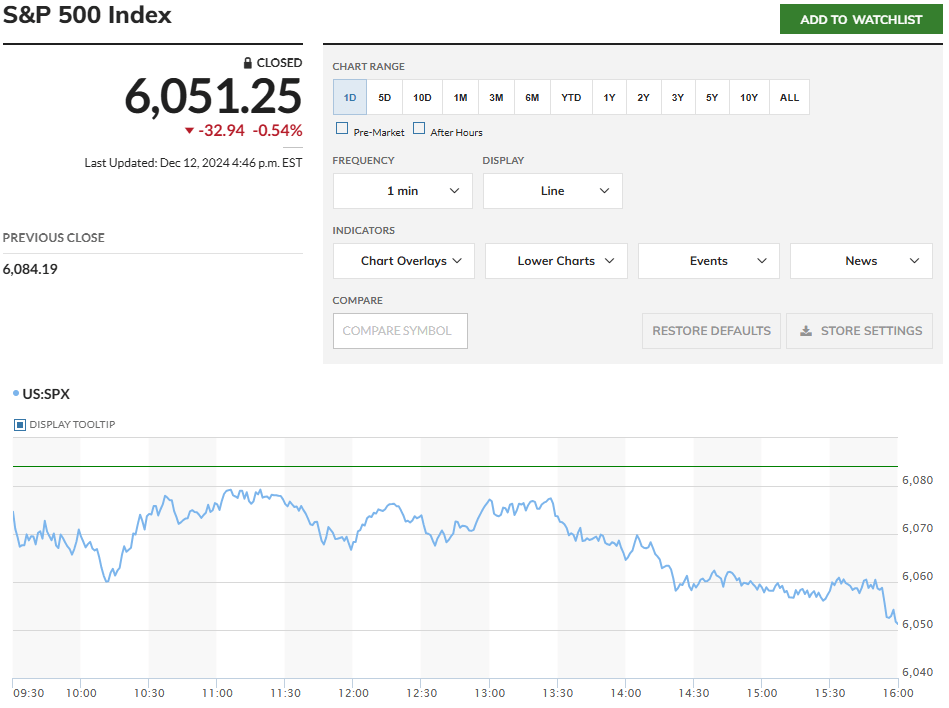

- In the U.S., the Producer Price Index (PPI) was a significant miss (3.0% vs. the expected 2.6%), and Initial Jobless Claims were also higher than anticipated (242K vs. 220K). Despite this, the FX market showed a muted reaction at the number but Dollar appreciation followed after the US Market Open. These developments contributed to a pullback in U.S. equities following the Nasdaq’s record close yesterday.

- The market’s focus for the Federal Reserve’s easing cycle has shifted to January, with the odds of another 25 basis point rate cut edging slightly higher to 22.3% (up from 20.8%). Meanwhile, a December 25 basis point rate cut remains fully priced in.

- President Elect Trump rang the bell at the NYSE during the market open. In a subsequent conversation with CNBC, he reiterated several points about tax cuts, tariffs, China policy, and cryptocurrency. These comments triggered a 30–40 pip USD depreciation across the board due to the inflationary pressures these policies could generate.

- Following the ECB rate cut, weak U.S. PPI data, and Trump’s remarks, the USD initially depreciated. However, after the options expiry at 10:00 AM, USD appreciation resumed and continued through the market close.

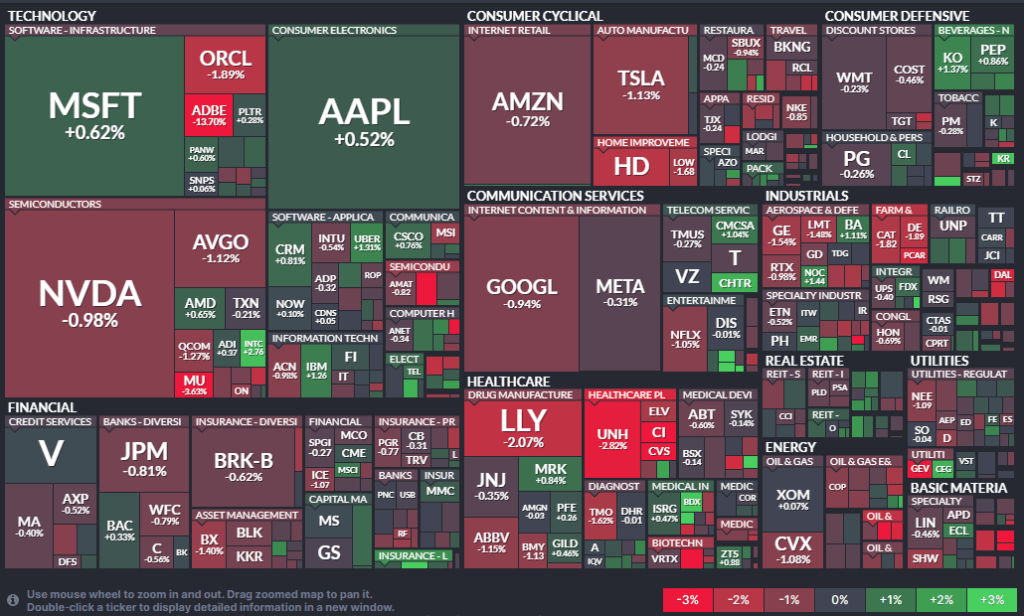

- Adobe’s stock fell 15% following weaker-than-expected growth forecasts for 2025 shared during its earnings call yesterday.

- Broadcom (AVGO) surged nearly 11% in after-market trading following its earnings report released after the close. The company beat EPS estimates but missed revenue expectations. However, a strong 3x revenue growth from AI business likely bolstered investor confidence.

- Costco (COST) also reported earnings after the market close, beating both EPS and revenue expectations. This performance underscores the resilience of U.S. retail buying power.

Tomorrow Outlook:

- I expect tomorrow to be a very slow day, as the focus has shifted to next week’s anticipated Fed rate cut. Next week will be the last full trading week before holiday liquidity kicks in, so the close after next week is likely to reflect the year-end values.

- USD appreciation has been the dominant macro trend—initially driven by the slower Fed easing cycle and now further amplified by Trump’s U.S. election victory. For this trend to reverse, the U.S. economy would need to deliver significantly weaker data to alter both the Fed’s outlook on rate cuts and the market’s view of the economy’s resilience. Otherwise, this trend could very well extend into the next year.

News Tomorrow(12/13): UK GDP at 2:00 AM, EU member states CPI at 3:00 AM and UK Consumer Inflation Expectations at 4:30 AM

Sources: Marketwatch(https://www.marketwatch.com/), , Reuters(https://www.reuters.com/), finviz(https://finviz.com/), fedwatch-tool(https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html), Tradingview(https://www.tradingview.com/)

Leave a comment